Restaurants Navigate the Road to Recovery

A. Elizabeth Sloan

A. Elizabeth Sloan

Food Technology Magazine

With almost 1 million U.S. foodservice locations and 15.6 million employees, the restaurant industry has been battered by the COVID-19 pandemic (NRA 2020a). As of June 30, 2020, restaurant job losses exceeded 5.5 million; 7.4% of U.S. restaurants were temporarily closed, and 3.5% had permanently shut down. Urban restaurants, which lost a key customer base as employees shifted to working remotely, were hardest hit (NRA 2020b, Datassential 2020a). In the first five months of the pandemic (March to July 2020), sales at restaurant and non-restaurant foodservice outlets (which include those at hotels and academic institutions) plunged by $165 billion and were headed for a decline of $250 to $300 billion in 2020 (NRA 2020a).

By late April, only 24% of all U.S. eating occasions involved some food or beverages sourced from a restaurant, including takeout and delivery (Hartman 2020). As of early June, 70% of U.S. households still prepared 80% or more of meals for all household members at home, compared with 40% who made that many meals at home prior to the COVID-19 crisis (IRI 2020a).

Americans are still primarily home-based. In mid-August, 29% went to work or school as normal, 33% worked/schooled remotely, and 38% were not working (Datassential 2020b).

With a secondary rise in COVID-19 cases this summer, the percentage of consumers very concerned about coronavirus returned to levels not seen since early in the pandemic. In mid-August, 62% were very concerned and 31% were somewhat concerned about it (Datassential 2020b). In a similarly pessimistic vein, as of midsummer, 39% of consumers thought that the coronavirus crisis would last more than one year (IRI 2020b).

While health concerns remain the top priority, economic worries are also growing, which is another factor likely to influence decisions about dining out.

Nearly half of U.S. adults were still avoiding eating out in mid-August, up 26% versus mid-March; 32% were nervous but still ate out, up 7%; and 22% had no concerns whatsoever, down 19% (Datassential 2020b). Boomers were most likely to avoid eating out; Gen Z consumers were the least likely to do so, Datassential reports.

While health concerns remain the top priority, economic worries are also growing, which is another factor likely to influence decisions about dining out. In mid-August, cutting back on restaurant spending and clothing were the primary ways consumers tried to economize. Nearly a third (32%) reported adhering to a specific budget, and 53% were watching prices more closely (Datassential 2020b).

But it’s not all doom and gloom. As of mid-August, nearly all forms of dining enjoyed double-digit growth in traffic versus May of this year, led by carryout meals. Nearly three-quarters (72%) of adults got restaurant food from a drive-thru, up 13%; 62% purchased takeout from an inside counter, up 14%; 57% made curbside/walk-up takeout purchases, up 7%; and 52% had restaurant fare delivered, up 15%. Four in 10 consumers dined inside a restaurant, up 23%; 34% dined outside (Datassential 2020b).

Customer transaction declines at major U.S. restaurant chains improved into the single digits for the week ended Aug. 16, 2020, after 21 weeks of double-digit sales declines, down 9% versus the same period last year but a significant gain from the steepest decline of 44% for the week ended April 12, 2020 (NPD 2020a).

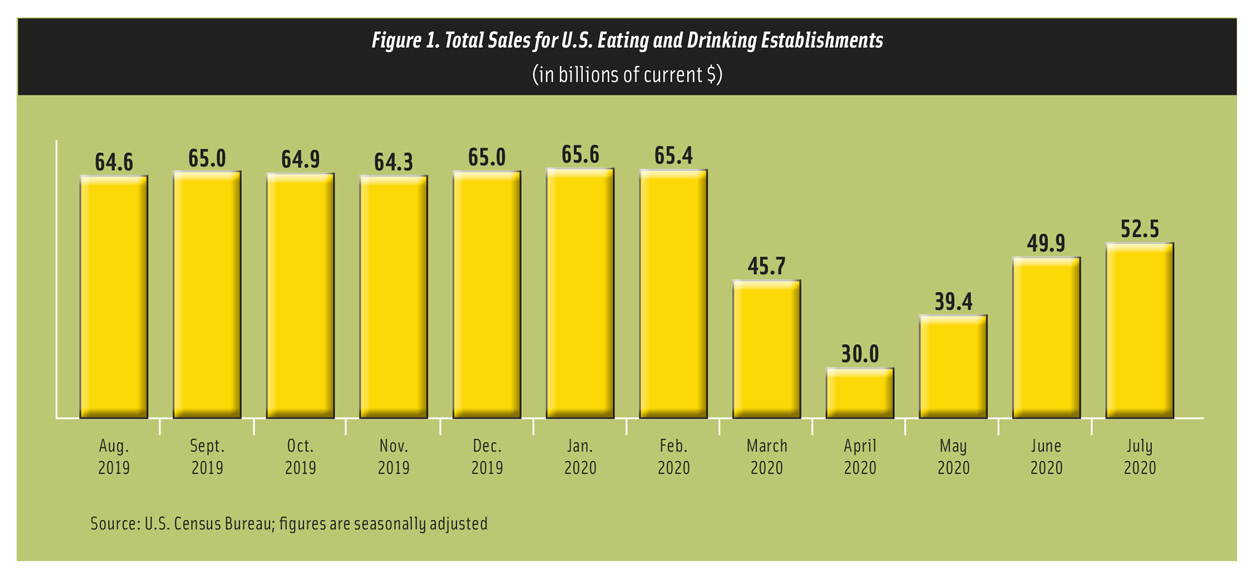

In July, total sales at eating/drinking establishments reached $52.5 billion, up 5% versus the prior month, although the gains were lower than those registered in May (31%) and June (27%) as reopening plans were again paused in some parts of the country (NRA 2020a, Figure 1).

Figure 1. Total Sales for U.S. Eating and Drinking Establishments (in billions of current $)

Source: U.S. Census Bureau; figures are seasonally adjusted

It’s clear to restaurateurs that the road to recovery will be challenging, however. Half of fine dining operators surveyed in July predicted that it will be more than six more months before traffic would be back to normal, barring any further issues. Four in 10 casual dining restaurateurs, one-third of fast casual and midscale dining operators, and one-quarter of quick-service restaurant (QSR) operators shared those sentiments (Datassential 2020c).

Not all restaurant sectors are weathering the pandemic storm equally well. For the second quarter ending in June, full-service restaurant traffic declined by 47% versus the same quarter a year ago while QSR traffic declined by 17% (NPD 2020b). Not surprisingly, recovery continued at a quicker pace for QSR chains. For the week of Aug. 15, 2020, transactions in QSR restaurants were down 8% versus the same week a year ago. Transactions at full-service chains, still impacted by dine-in closings, fell 19%, but still a major positive gain from their steepest decline of 75% for the week ended April 12, 2020 (NPD 2020a).

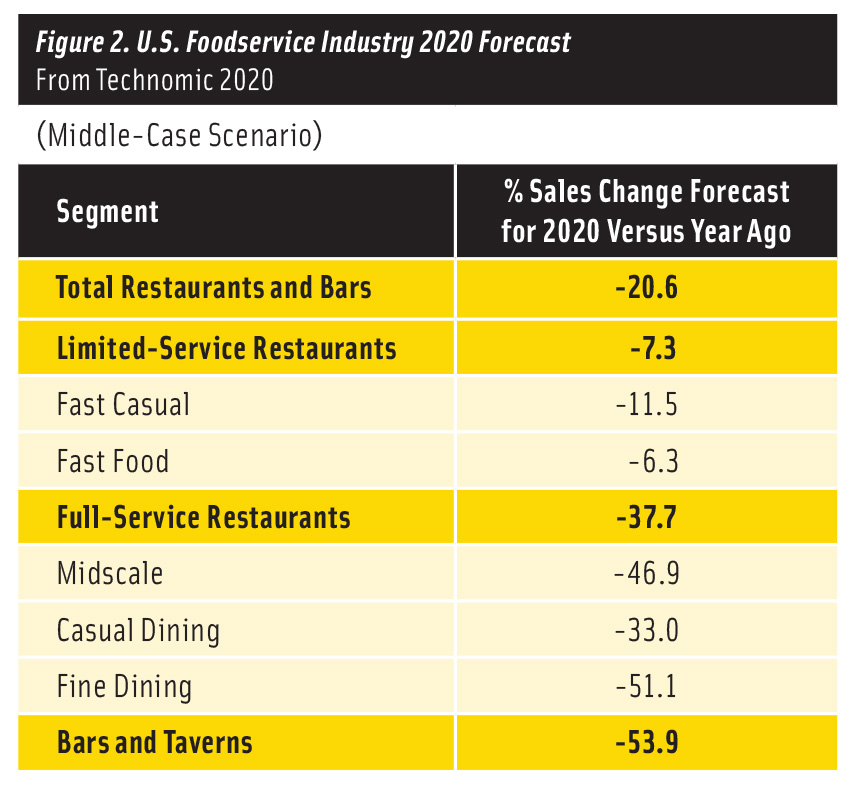

In mid-August, Technomic released its 2020 foodservice industry sales forecast as a three-tier best-worst-middle-case scenario. Per Technomic’s middle-tier scenario, limited-service restaurant sales are forecast to be down 7.3% by the end of 2020 while sales in full-service restaurants are expected to be down by 37.7%. Bar/tavern sales are projected to decline by 53.9% (Technomic 2020a). (See Figure 2 for more details.) Technomic has revised its 2021 foodservice industry forecast, projecting industry growth of 21% in 2021, with overall sales still down 11% from 2019 (Technomic 2020b).

Figure 2. U.S. Foodservice Industry 2020 Forecast

From Technomic 2020

Chain Restaurant Update

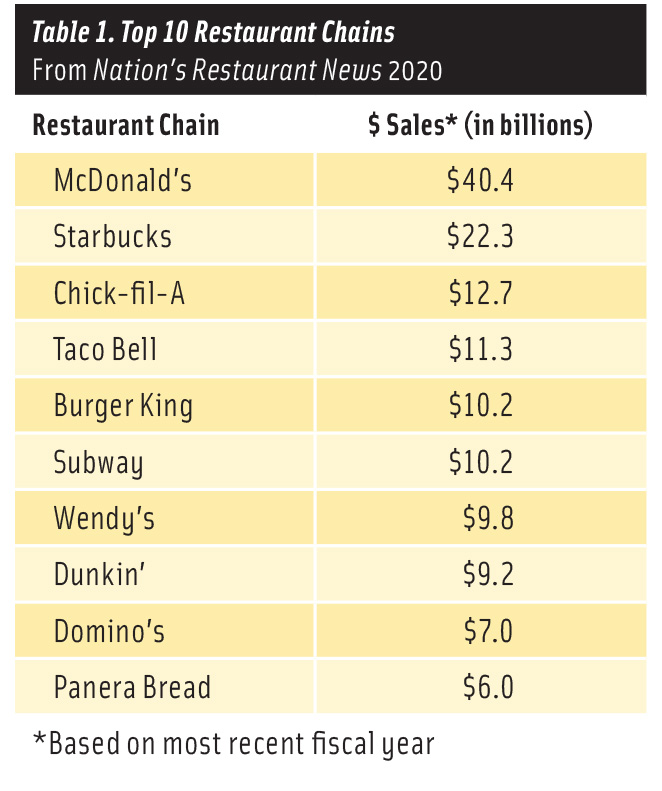

McDonald’s remains the largest U.S. restaurant chain, with total sales of $40.4 billion, followed by Starbucks Coffee and Chick-fil-A, which moved into the No. 3 position last year. Subway dropped from No. 4 to No. 6. Popeyes is now among the top 20 chains (Nation’s Restaurant News 2020). (See Table 1 for the full top 10 list.)

Table 1. Top 10 Restaurant Chains

From Nation’s Restaurant News 2020

Among the top 200 chains, Shake Shack posted the fastest growth, followed by First Watch, MOD Pizza, Raising Cane’s Chicken Fingers, Tropical Smoothie Café, Lazy Dog Restaurants, Chick-fil-A, Wingstop, Cooper’s Hawk Winery & Restaurant, and Popeyes. All had double-digit growth ranging from 18% to 34% (Nation’s Restaurant News 2020).

Limited-service burger restaurants account for the largest share of sales among the top 200 chains, 28.3%. The breakout also includes casual dining restaurants, accounting for 15.5% of sales; beverage/snack restaurants, 11.7%; chicken restaurants, 9.6%; pizza chains, 7.8%; limited-service sandwich restaurants, 7.0%; limited-service Mexican restaurants, 6.6%; and family dining, 5.1% (Liddle 2020).

Chicken was the fastest-growing menu segment in terms of sales,followed by beverage/snack, limited-service Mexican, limited-service burger, bakery/café restaurants, and limited-service specialty restaurants, led by Panda Express, Captain D’s Seafood Kitchen, and Noodles & Company (Liddle 2020).

Sales at Wingstop jumped 31.9% for the second quarter of 2020. Other chains recording strong growth for the quarter included Popeyes, up 28.5%; Papa John’s, +28.0%; Domino’s, +16.1%; KFC, +7.0%; and Pizza Hut, +5.0% (Technomic 2020c).

Seventy percent of restaurant traffic in the QSR and coffee/snack segments was off-premise in 2019, so it’s not surprising that half of fast casual chains and 20% of family dining and casual dining establishments have focused on upgrading their drive-thru, delivery, and takeout programs (NRA 2020c, Luna 2020a).

Solutions and Opportunities

At the same time, operators have introduced a number of new mealtime solutions—from family-sized offerings to pre-prepared meals—that may remain longer-term opportunities.

With millennials with children being the fastest-growing group of restaurant users over the past two years and 41% of food consumer product growth coming from households with kids during the pandemic, family meal bundles and promotions have been well-received (Technomic 2018a, IRI 2020a).

The idea for do-it-yourself doughnut kits originated at a California Dunkin’ franchise as a way to help entertain kids sheltering in place and soon spread to franchisees across the country. Photo courtesy of Dunkin’

Four in 10 diners have already tried a family meal bundle, and 26% would like to. Of those who bought them, 80% would do so again. While comfort/classic dishes are the most popular, healthy and diet meals are the fastest growing. Just over one-third of consumers would like to see more globally inspired and chef-inspired family meal options (Datassential 2020b).

Two-thirds of consumers would also like family meal bundles for dayparts other than dinner, especially millennials and those in upper-income households (Datassential 2020a). Carl’s Jr. offers both breakfast and lunch family bundles that will feed up to four for $15.

In addition, 41% of diners say they’ve tried heat-and-eat and take-and-bake restaurant meals; 36% have tried a fresh meal kit from a restaurant. Although a high percentage of buyers say they’ll order them again, about half feel they’re too much work or often are overpriced (Datassential 2020b).

Of those interested in these more hands-on items, six in 10 would like build-your-own pizza, tacos, or burrito kits, pre-prepped barbecue kits, ready-to-grill restaurant steaks, take-and-bake desserts, and signature seasonings/sauces. About half are interested in decorate-your-own dessert or cocktail kits (Datassential 2020b).

A limited-time offering introduced this spring in time for Cinco de Mayo, Taco Bell’s At Home Taco Bar bundled all the fixings for feeding a group of six for $25. Photo courtesy of Taco Bell

Taco Bell offered a limited-edition At Home Taco Bar kit for $25. Cracker Barrel has Family Meal Baskets To-Go and Take n’ Bake sides and entrées. Dunkin’ kits allow for do-it-yourself doughnut decorating; Friendly’s has sundae kits that promise to “keep the kids occupied with an edible art project.”

Marrying iconic restaurant brands with food retail has long been a very successful practice. For the 12 weeks ending May 17, 2020, versus the same period a year ago, P.F. Chang’s brand multiserve frozen meal sales jumped 96%, per IRI. Menchie’s Frozen Yogurt recently introduced frozen yogurt varieties in Hi-Chew candy flavors.

Although more than one-third of diners report that they’ve bought grocery/pantry staples at a restaurant, nearly two-thirds view them as overpriced (Datassential 2020b). Signature sauces, seasonings, coffee/tea, and baked items may be exceptions. Subway grocery essentials are available in more than 1,500 Subway restaurants in 35 states (Glazer 2020).

Virtual, cloud, or ghost kitchens are another fast-emerging phenomenon where all food is prepared in a commercial cooking space to be picked up or delivered. Research and consulting firm Foodservice IP forecasts that ghost restaurant sales will increase 42% in 2020 (Luna 2020b).

Restaurant wine clubs are another business builder. Cooper’s Hawk Winery & Restaurants have over 450,000 wine club members (Glazer 2020).

Menu Makers

Two-thirds of consumers are tired of cooking at home, 58% are bored with comfort foods, and 79% are craving something new—and that’s good for the restaurant business (Datassential 2020b).

Craveable favorites, globally inspired dishes, foods that are difficult to make at home, and purely indulgent treats are among the top motivators prompting consumers to return to restaurants (Datassential 2020b). Consumers reported missing Asian and Mexican dishes while at home, per Datassential.

With pizza, sandwiches, burgers, pasta, rice, French fries, mac and cheese, and chicken nuggets the foods consumers have grown tired of eating during the pandemic, upgrading these staples is a foolproof strategy for foodservice operators (Datassential 2020d).

American regional flavors rank third among the hot cuisine trends for 2020 (NRA 2019). Wienerschnitzel serves hot dogs in Texas and Kansas City varieties. KFC offers Georgia Gold Fried Chicken.

TGI Fridays introduced a Guinness Pub Burger. Domino’s just debuted a Memphis BBQ Chicken Pizza, and Rapid Fired Pizza offers a Smoky BBQ Chicken Pizza. Menu developers might substitute ethnic sausage in tacos or top load fries with Korean or Indian sauces/stews for a unique ethnic poutine.

Rapid Fired Pizza keeps it interesting with a Smoky BBQ Chicken pizza. Photo courtesy of Rapid Fired Pizza

Switching out chicken for affordable seafood is another option for adding interest to menus. White Castle has Siracha Shrimp Nibblers on the menu, Church’s Chicken has new fried seafood platters, and Del Taco offers a Beer Battered Shrimp Taco.

Expect family comfort favorites that require more lengthy preparations and expense, such as Cracker Barrel’s Pot Roast Dinner and Barrel-cut Sugar Ham, to get the nod.

Cheesy, followed by savory, sweet, buttery, and spicy, are the most craveable flavors (Technomic 2019). Technomic reports that half of consumers like very spicy foods, and 48% of Southerners crave tangy flavors.

While dine-in patrons (51%) are most likely to try new flavors, 37% experiment with flavors for takeout/carryout, and 31% get experimental with delivery orders. Millennials are most likely to do so (Technomic 2019). Four in 10 diners consider a twist on a familiar flavor, a regional or local flavor, or a fusion flavor of multiple cuisines to be unique, according to Technomic data.

While plant-based burgers and avocado toast top the list of items posting exceptional growth on menus over the past four years, some ethnic preparations aren’t far behind, including Cacio E Pepe, Hot Chicken, Tinga, and Chicken Pad Thai (Datassential 2020e).

Asian Island (e.g., Indonesian), South American, regional Chinese, and Indian are other trendy ethnic table-service cuisines for 2020 (NRA 2020c). Half (51%) of U.S. adults have tried and liked Sichuan, 42% are fans of Hunan, and 48% like Cantonese cuisine (Technomic 2018b). The Pei Wei chain has kept pace by offering Spicy Korean BBQ Steak and a Thai Basil Rice Bowl.

Japanese milk bread, Brazilian pão de queijo, Persian barbari, and Indian chapati and poori are among the unique ethnic breads setting the pace in fine dining (Datassential 2020e).

Nashville hot, tajin, gochujang, furikake, matcha, pink peppercorn, and pitaya were among the fastest-growing flavors on menus over the past four years (Datassential 2020d). Filfel chuma, palapa, huli, pilacea, and jaew bong are up-and-coming ethnic sauces (Technomic 2019).

Lesser-known mushrooms, new rabes (e.g., collard, caulilini), new shoots/sprouts (e.g., hops), and kale hybrids will be among the unique produce items grabbing diners’ attention (NRA 2019).

More than half of restaurant operators report that patrons are ordering fewer alcoholic beverages, desserts, appetizers, and nonalcoholic drinks since the pandemic began. Increasing orders in these menu segments should be a top priority (Datassential 2020f).

Elote (Mexican corn), fried cauliflower, and cobb dip have enjoyed triple-digit growth on appetizer menus over the past four years; cheese curds, arancini, burrata, and chicharrón (fried pork belly or pork rinds) have grown by more than 50% (Datassential 2020e).

Snack-sized items and mini desserts were among the items projected by QSR and fast casual operators to become even more popular on menus in 2020 (NRA 2020c). Churros, beignets, affogato, mochi, and pot de crème are ethnic additions to dessert menus with high sales potential; they’ve increased in frequency on menus from between 30% and 50% over the past four years (Datassential 2020e).

Boozy treats, dairy-free frozen desserts, drinkable desserts, and herb-based sweets are other trendy desserts for 2020 (NRA 2019). Wild Berry Cobbler from Church’s Chicken marries a fruity dessert sauce with its signature Honey-Butter Biscuits.

Kombucha, agua fresca, fruit/veggie milks and specialty drinks, sparkling waters/seltzers, and boba/bubble teas are nonalcoholic beverage currently trending (NRA 2019). Nitrogenating and adding extra carbonation are also on trend in the beverage category (Thorn 2020).

Exclusive limited-time beverage offerings like Mtn Dew Summer Shock from PepsiCo and the Bojangles restaurant chain are grabbing customer attention. Del Taco marries boba and soda in its Sprite Poppers.

Half of fast casual restaurants have expanded their delivery options to cater to consumers during the pandemic. © Sasha_Suzi/iStock/Getty Images Plus

Although the legality varies by jurisdiction, alcohol delivery is a growth opportunity with high potential for restaurants. More than half (56%) of adults say they would likely order alcoholic beverages as part of a restaurant meal delivery order; for millennials, that percentage is 79% (NRA 2020c).

Alcoholic seltzers, Aperol spritzers and other spritzers, mezcal varieties (e.g., sotol and raicilla), and Asian spirits (e.g., baijiu, soju, and shochu) are among the trendy spirits for 2020 (NRA 2019).

The pandemic has also reprioritized dayparts for foodservice operators; dinner is now the top restaurant occasion (Technomic 2020c). In June, 23% of restaurant patrons ordered dinner; 16%, lunch; 8%, breakfast; and 5%, a snack. Breakfast and morning snacks have suffered the steepest declines (NPD 2020c).

Ethnic breakfast dishes rank fifth among the overall hot culinary trends for 2020 for table-service restaurants (NRA 2020c). Chicken and waffles, tostadas, nachos, and churros have enjoyed explosive growth on early morning menus (Datassential 2020d).

With millennials and Gen Z consumers significantly most likely to use restaurants and also the most likely to have upgraded their cooking skills during the pandemic, staying ahead of trends and offering their favorite foods is imperative (Hartman 2020, FMI 2020). Sushi, barbecue pizza, Korean barbecue, buffalo chicken, ramen, and smoothie bowls are among the younger generation’s favorites (Datassential 2020b).

Plant-based proteins, healthy bowls, specialty burger blends (e.g., mushroom and beef combinations), and unique beef/pork cuts are projected to be top of mind for table-service chefs this year (NRA 2020c).

Leaning Into Healthy Options

Since the advent of COVID-19, 43% of U.S. adults say they have changed their diet to eat healthier (IFIC 2020). Eight in 10 adults are more likely to choose a restaurant if it offers healthy options (NRA 2020c).

Natural ingredients, minimally processed foods, fruit/vegetable sides for kids’ meals, and gluten-free, vegetarian, vegan, locally sourced, and organic offerings are among the menu items QSR and fast casual operators projected would become more popular in 2020 (NRA 2020c).

The presence of young children in a household is a significant motivator for healthy eating. Kid-specific healthy menus have become increasingly important as parents make separate meals for adults and kids on 49% of family eating occasions (FMI 2019). Households with kids are among the most likely to have increased their use of plant-based foods (FMI 2020). For the year ended May 2020, 28% of adults report eating more plant-based foods, 24% are consuming more plant-based dairy alternatives, and 17% are opting for more plant-based meat alternatives (IFIC 2020).

A pseudo-vegan movement is sweeping the nation. One-third of adults say they are very interested in vegetarian foods, and 28% are very interested in vegan foods, although only 5% are strict vegetarians and 3% are vegans (Datassential 2019). Vegan descriptors for restaurant desserts are up 21.8% over the past year; vegan burger mentions are up 18.3% (Technomic 2020d).

Warm bowl meals are an increasingly popular option among diners seeking to eat healthfully.

© vaaseenaa/iStock/Getty Images Plus

Veggie-centric fare may well be a larger opportunity than vegetarian or vegan options. Nearly nine in 10 millennials and Gen Zers (88%) want more plant-based items featured as ingredients in their foods (Culinary Visions 2018). One-third of consumers most associate plant-based eating with consuming more fruits and vegetables (Hartman 2019).

Edamame noodles, lentils, and farro are among 2020’s hot substitutes for traditional grain-based pasta products (NRA 2019). Mushrooms, pulses, and new varieties of chili peppers have been recast as on-trend flavors for 2020.

With current consumer preferences shifting to warm versus cold foods, green salads are increasingly giving way to produce-centric bowl meals (Datassential 2020a). The Chopt Creative Salad Co. has introduced warm salad look-alike bowls such as Asian Chopped Chicken Bowl.

The Iced Pineapple Matcha Drink is among an extensive array of nondairy products that Starbucks serves up. Photo courtesy of Starbucks

Grilled and marinated cheese are showing up at the center of the plate in place of meat. Desserts, dips, creamers, and butter and cheese alternatives are among the fastest-growing plant-based categories (IRI 2019). Hybrid drinks of milk and nondairy milk alternatives are another fast-emerging trend.

In mid-April, 43% of consumers said they tried a diet plan during the past year; among those aged 18–34, 58% did so. Of the 43%, 9% experimented with clean eating; 8%, keto/high-fat diets; 7%, low-carb diets; and 6% each, carb cycling, gluten-free, or the Mediterranean diet (IFIC 2020).

Targeting the calorie conscious, Pollo Loco launched a menu of offerings with fewer than 500 calories. And Yogurtland introduced light ice cream in an Organic Blossom Peach flavor.

Four in 10 consumers (42%) say that they opt for unique foods and ingredients when trying to eat healthy (FMI 2020). Superfoods such as matcha, goji, edamame, turmeric, black garlic, dragon fruit, heirloom vegetables, and avocado oil have enjoyed triple-digit growth on restaurant menus over the past four years (Datassential 2019).

Not surprisingly, with COVID-19 focusing attention on at-risk individuals, functional foods are becoming more influential in foodservice. Heart health, energy, weight management, and gut health are high-priority issues for many restaurant patrons (Datassential 2018).

Keeping It Safe and Sound

COVID-19 has ushered in a new era of food safety at restaurants; consumers now consider safety as important as taste when dining out. Four in five say the presence of proper safety practices impacts their restaurant choice (Datassential 2020a). As of mid-July, nine of 10 operators had upgraded their food safety procedures and said that they will maintain these practices post-pandemic (Datassential 2020f).

In descending order, restaurants with outdoor seating, QSRs, and grocery deli/prepared food departments are the foodservice venues consumers would feel most safe using; fast casual restaurants, coffee shops/cafés, convenience stores, fine dining restaurants, and hotel room service were cited by more than half of consumers. Four in 10 would visit a food truck or use catering, 35% would go to a bar or tavern, and 33% are comfortable in food courts. Buffet restaurants are not in the comfort zone for most; just over a quarter of diners (28%) say they feel safe visiting them (Datassential 2020f).

For now, coronavirus remains the world’s greatest worry, with 55% of global consumers placing it among their top three concerns (Ipsos 2020). For restaurateurs, there can be little doubt that its impact remains a grave concern, particularly as winter approaches, limiting outdoor dining options in many locations.

REFERENCES

Culinary Visions. 2018. Ethnics on the Go. Culinary Visions Panel, Chicago. culinaryvisions.org.

Datassential. 2019. Functional Foods. Datassential, Los Angeles. datassential.com.

Datassential. 2020a. The Road to Recovery.

Datassential. 2020b. “The Simply Smarter Webinar: EP4—Innovation Inspiration.” Webinar, Aug. 21.

Datassential. 2020c. Operators Dig In.

Datassential. 2020d. One Table Survey.

Datassential. 2020e. MenuTrends Update.

Datassential. 2020f. “Game On . . .” Webinar, June 19.

Datassential. 2020g. “The Magnificent Seven.” Webinar, June 26.

FMI. 2019. U.S. Grocery Shopper Trends. Food Marketing Institute, Alexandria, Va. fmi.org.

FMI. 2020. Grocery Shopper Trends—Cooking.

Glazer, F. 2020. “Restaurants change course to stay afloat during coronavirus crisis.” Nation’s Restaurant News 54(8): 16, 17.

Hartman. 2019. Health + Wellness 2019: From Moderation to Mindfulness. The Hartman Group, Bellevue, Wash. hartman-group.com.

Hartman. 2020. “COVID-19’s Impact on Eating.” Webinar, Aug. 11.

IFIC. 2020. Food & Health Survey. Intl. Food Informa-tion Council, Washington, D.C. foodinsight.org.

Ipsos. 2020. What Worries the World: Ipsos Global Advisory Survey. Ipsos, Paris. ipsos.com.

IRI. 2019. “The Surge of Plant-based Foods.” Webinar, Nov. 16. IRI, Chicago. iriworldwide.com.

IRI. 2020a. “Charting the Course for Continued Center Store Growth.” Webinar, June 16.

IRI. 2020b. “How COVID-19 is Reinforcing and Re-shaping Fresh Foods.” Webinar, August 26.

Ipsos. 2020. What Worries the World: Ipsos Global Advisory Survey. Ipsos, Paris. ipsos.com.

Liddle, A. 2020. “Top 200 post sales growth as coronavirus’ full impact looms.” Nation’s Restaurant News 54(8): 30, 32, 33.

Luna, N. 2020a. “Drive-thrus put these chains in the fast lane of recovery.” Nation’s Restaurant News 54(8): 10–11.

Luna, N. 2020b. “Chains look to ghost kitchens, virtual brands to drive sales.” Nation’s Restaurant News 54(8): 12–14.

Nation’s Restaurant News Staff. 2020. “Meet the Top 200 chains in America.” Nation’s Restaurant News,

June 11. nrn.com.

NPD. 2020a. “U.S. Restaurant Chain Transaction Declines Improve into Single-Digit for the First Time Since March.” Press release, Aug. 25. The NPD Group, Chicago. npd.com.

NPD. 2020b. “The Struggle is Real for U.S. Full-service Restaurants as Visit and Transaction Declines Stay in the Double Digits.” Press release, July 30.

NPD. 2020c. “U.S. Restaurant Chain Transaction Declines Continue to Soften, Down -14% in Week Ending June 7.” Press release, June 15.

NRA. 2019. What’s Hot Culinary Forecast 2020. National Restaurant Assoc., Washington D.C.

restaurant.org.

NRA. 2020a. “Restaurant sales continued to rise in July, but at a much slower pace.” Press release,

Aug. 14.

NRA. 2020b. “Restaurant job growth slowed significantly in July.” Press release, Aug. 7.

NRA. 2020c. State of the Restaurant Industry.

Technomic. 2018a. Generation Consumer Trend Report. Technomic, Chicago. technomic.com.

Technomic. 2018b. Ethnic Consumer Trend Report.

Technomic. 2019. The Flavor Consumer Trend Report.

Technomic. 2020a. U.S. Foodservice Industry Technomic Forecast 2020. Updated by Joe Pawlak.

Technomic. 2020b. “Technomic Revises Industry Forecasts.” Press release, Aug. 12.

Technomic. 2020c. Industry Insights, Aug. 10.

Technomic. 2020d. Industry Insights, July 27.

Thorn, B. “7 Beverage Trends to Watch.” Nation’s Restaurant News 54(2): 47-49.

Hero Image: MARIA PAVLOVA

Authors

-

A. Elizabeth Sloan President

A. Elizabeth Sloan, PhD, is CEO and president of consumer trends consultancy Sloan Trends Inc. and a longtime contributing editor of Food Technology magazine. A veteran of work in industry, media, and public relations, Sloan received a PhD in food science and technology from the University of Minnesota.

Categories

-

Food Business Trends

-

Foodservice

-

Consumer and Marketplace Trends

-

Food Technology Magazine