Startup Lessons Learned

Mary Ellen Kuhn

Mary Ellen Kuhn

Food Technology Magazine

Eight years ago, seeking a healthier way to eat, Katlin Smith developed three clean label baking mixes while working as a management consultant.

Katlin Smith of Simple Mills

“Once that was done,” says the founder and CEO of natural foods company Simple Mills, “I liquidated my personal savings, accepted my parents’ offer to reverse-mortgage their home to raise additional funds, mixed and packaged the products myself at night, and ultimately quit my job so that I could get Simple Mills off the ground.” Today, she says, Simple Mills is the market leader in the natural channel’s baking mix and cracker categories and has a strong presence in mainstream grocery and mass merchandise chains, including Kroger, Walmart, and Target.

“In the beginning, I could not get meetings with key grocery buyers, so I traveled to major markets dragging multiple suitcases with me—frequently taking buses and staying in hostels to save money—and baked batches of muffins that I dropped off in cold calls,” Smith continues. “Without that full-time commitment, there would be no Simple Mills today.”

Smith’s commitment is not necessarily the norm. When aspiring entrepreneurs tell startup consultant Jeff Grogg of JPG Resources that they’re going to launch their new food or beverage brand by working nights and weekends, he shares a hard truth: “No, you’re not.” It’s going to take a lot more than that, he stresses.

“The common theme with starting a company is that it’s so much harder than people expect it to be,” says Grogg. “It’s going to be 80 hours, 100 hours a week. It’s just full on all the time. You have to be willing and able to be that committed.”

“Most successful startups take seven to 10 years to really get to scale,” says Greg Bunch, who teaches entrepreneurship at the University of Chicago Booth School of Business and counts Smith among his former students. “Most people don’t have the patience to spend seven to 10 years building a business. They might be better suited to keeping their day jobs.”

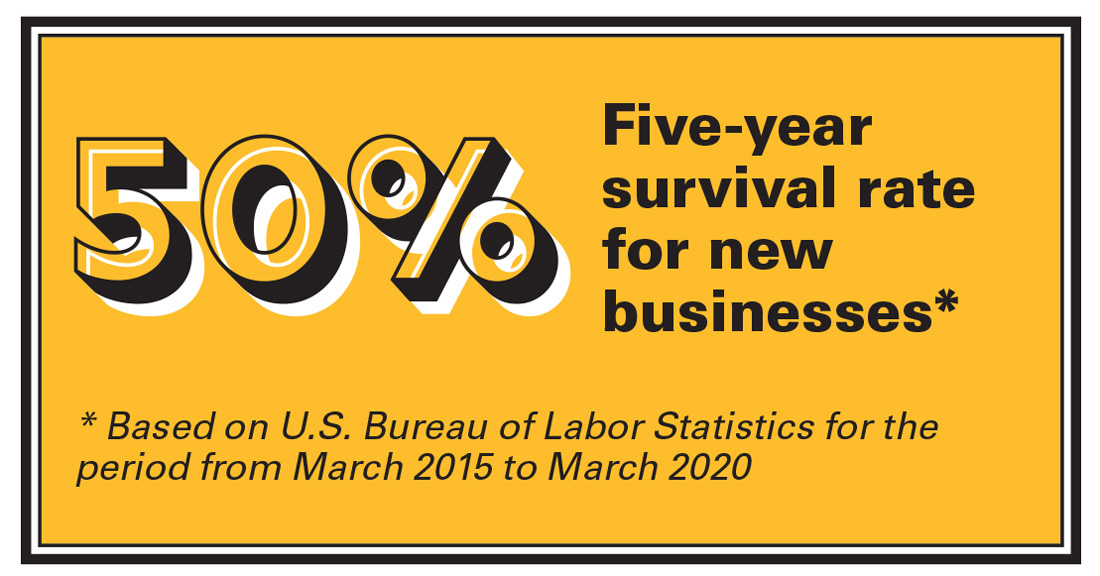

Entrepreneurs face a high-stakes game. The five-year survival rate for new businesses is 50%, according to the U.S. Bureau of Labor Statistics.

Sweat equity alone is not enough to counter that statistic. What else does it take to achieve startup success? We turned to the experts—investors, mentors, and savvy founders—for answers. Here’s their collective wisdom distilled into nine essential truths.

1. Make sure you’re solving a problem.

Consider ag tech entrepreneur Matthew Rooda, who identified the problem of “piglet crushing” while working as a farrowing manager during his college years. Rooda was frustrated because he’d arrive at the farm each morning and find dozens of baby pigs crushed to death because sows had lain on top of them shortly after birthing them.

“We had to make a thousand failures to come up with a success.”

Rooda did some research and discovered that 92% of the pork producers he surveyed were seeking a solution to the same problem. He teamed with two co-founders to develop a device called SmartGuard that—when triggered by piglet squeals—prompts the sow to stand up, sparing the lives of the piglets. In the six years since its founding, their company, SwineTech, has raised about $6.3 million in venture capital and now offers a suite of products that add efficiencies and reduce mortalities in swine farrowing operations. SmartGuard alone lessens piglet crushing by up to 31%, SwineTech’s analysis shows.

Creating a product with strong success potential requires “systems thinking,” says Lauren Lackey, president and owner of Centauri Innovations, a new product development and R&D consultancy. “First, you’ve got to figure out what the struggle is, and then you’ve got to design the end-to-end experience to match that problem.”

Too many founders fall into the “field of dreams” trap, thinking that “if we build it, they will come,” Lackey continues. “That’s not true. Just because you build it does not necessarily mean that they will come.” It’s only true if the product addresses an unmet consumer need, she emphasizes.

2. Less is more. Stay focused.

Startups that try to do too much too soon can flounder, says Darren Streiler, who identifies up-and-coming innovators as investment director for Archer Daniels Midland’s venture capital arm, ADM Ventures. “It’s really vital to have a strong focus before expanding just to allow for greater control and opportunities for growth,” says Streiler.

Bunch recommends keeping a careful eye on the “beachhead customer” at the outset. He cites the example of RXBAR co-founders and CrossFit exercisers Peter Rahal and Jared Smith, who initially “got micro-focused” on their target audience of CrossFit gym patrons. The two “became mainstays on the CrossFit circuit, pushing product one bar, one box at a time,” according to the founders’ story on the RXBAR website. After spending a year “getting it right,” they expanded their sales efforts and eventually sold the protein bar company to Kellogg’s for $600 million.

Streiler points to French biotech startup InnovaFeed, a supplier of insect-derived animal feed, as another example. The company is building an insect protein operation adjacent to an ADM corn processing complex that will supply it with feedstock. Streiler credits InnovaFeed’s founders with keeping their attention on the animal feed market as the company embarks on this new venture rather than simultaneously targeting the human food market. Trying to go after two such different markets would be challenging, he posits, because they operate very differently.

3. Timing matters (a lot).

Successful startups get the timing right—when the consumer is ready for the product but before the market is saturated. In fact, sometimes it’s better not being first.

“Post–Beyond Meat, it was a lot easier to get into the plant-based sector than pre–Beyond Meat,” says Sanjeev Krishnan, chief investment officer and managing director, S2G Ventures, a venture fund focused on food and agriculture entrepreneurs. “You have to time the zeitgeist of the consumer, the channel, [and] the access to capital.”

One of the companies in S2G’s portfolio is Once Upon a Farm, which debuted refrigerated baby food in pouches in 2015. Mounting consumer interest in fresh, healthful fare meant the shelf-stable baby food market was ripe for disrupting at that time, says Krishnan. Co-founder and CEO John Foraker “saw an opportunity to take a shelf-stable category like baby food and really make it fresh and differentiate it,” Krishnan notes.

Imperfect Foods’ average order size doubled over the prior year in 2020. Photo courtesy of Imperfect Foods

The COVID-19 pandemic has brought growth opportunities for Imperfect Foods, a home delivery purveyor of so-called “ugly produce” that can’t be sold via conventional retail channels.

“At the onset of the pandemic, we saw huge growth in new memberships as more people were avoiding in-person trips to the grocery store,” says Imperfect Foods CEO Philip Behn. “Being delivery-only and offering our own private label products, we already had a model in place that allowed us to serve customers when others couldn’t.” By the end of 2020, the company’s active user base had grown by 40% over the start of the year and weekly order volumes had doubled, Behn reports.

“They were there at the right time with the right idea” and “had the tools in place” for direct-to-consumer delivery, says Anne Greven, global head of food & agribusiness startup innovation at Rabobank.

4. The end result probably won’t look like the original idea.

Being open to input from retail customers and using it to refine the product concept is critical, says Patrick Henry, author of Plan Commit Win: 90 Days to Creating a Fundable Startup and CEO of GroGuru, an ag tech company. Such “teaching customers” help a company tweak its concept to make it more marketable, Henry notes.

Pivoting to service healthcare workers helped keep Farmer’s Fridge going even after COVID-19 reduced consumer traffic at many of its vending machine locations. Photo courtesy of Farmer’s Fridge

Krishnan says the same is true of the “early adopter cohort” of consumers. These customers “will let you make mistakes, help you scale, and be forgiving,” he explains. Lackey agrees, describing early misses as “just another set of data points.”

Rooda of SwineTech laughs when he describes his initial approach to tackling the piglet crushing issue. “We had a really bad idea to start with,” he says, explaining that it involved creating robotic piglets and conditioning sows to respond to their distress signals.

Fortunately, he sought the advice of in-the-field experts. “We went back and met with potential customers and bounced ideas off them,” says Rooda. Those conversations ultimately led the founders to the latest SmartGuard iteration, which uses a wearable monitor and gently alerts sows when their piglets are in peril, taking the animals’ natural intelligence and ability to learn into account.

Rooda and his team slogged through dozens of iterations to arrive at the final version, including one akin to training collars for dogs. “But surprisingly enough,” says Rooda, “a dog collar was too strong for a pig. So we worked with Kansas State University to figure out what is the right stimulus.”

5. Get flexible.

Winners get creative when market conditions change.

As an example, Greven cites Farmer’s Fridge, a 2018 Rabobank FoodBytes! award winner that pioneered the concept of selling salads in jars from refrigerated vending machines, installing the units in office buildings and airports.

The pandemic “could have really cratered a company like Farmer’s Fridge,” says Greven. “But within a month, they had completely retooled and used their processing facilities and their model to serve meals to frontline workers. The nimbleness—their ability to be flexible and to think about where their product was needed very quickly—has elevated them but also shown their ability to use their unique distribution model in a different way, which has worked for them.”

For Imperfect Foods, 2020 pivots allowed it to support “small producers who’ve been hit hard by the pandemic,” according to Behn. “For example, we sourced snack trays destined for JetBlue flights, popcorn destined for movie theaters, granola destined for college cafeterias, and so much more.”

And in keeping with its socially conscious mission, Imperfect Foods piloted emergency response programs during the pandemic. The company partnered with Kroger’s Zero Hunger Zero Waste Foundation to test a reduced-cost box program for those who qualify for the U.S. Department of Agriculture’s Supplemental Nutrition Assistance Program benefits and waived delivery fees for needy consumers over the age of 65.

6. You’re only as good as the team you build.

Sometimes it’s difficult for smart, intense founders to acknowledge that they need a support system, says Henry. But experts agree that creating a strong team is a recurring theme in business success stories. Henry notes that even brilliant entrepreneurs like Sergey Brin and Larry Page of Google or Mark Zuckerberg of Facebook had mentors and recognized the value of building a team.

“You [the founder] can’t have too much ego to own everything,” says Greven. She’s a fan of soil analytics company Trace Genomics, where Stanford PhD co-founder Poornima Parameswaran saw the importance of recruiting a seasoned business professional as CEO to complement her technical expertise. “The vision was hers, and she built the strengths underneath it to actualize it,” says Greven.

“Part of being a leader is you have to know the things you’re good at,” says consultant Grogg. And another, equally important part, he continues, is adding team members to handle “the things you’re less good at.”

Simple Mills’ Smith speaks candidly about the lessons she’s learned about building and managing a team. “My earliest employees were young and enthusiastic but not sufficiently knowledgeable about the CPG space to help me scale the business,” she says.

“I then hired veterans of companies like Kraft, General Mills, and PepsiCo, who saw the need for healthier packaged foods and committed to helping drive the change, but I ran into problems early on because I was micromanaging,” Smith continues. “With the help of an executive coach, I learned to lead rather than manage and to give people the leeway to figure things out for themselves.”

7. Velocity is king.

A new product won’t succeed if a startup can’t get retail distribution, of course. According to Grogg, however, focusing on distribution at the expense of velocity—the rate at which the product is moving off the shelf—is among the “classic mistakes” that startups make. “A lot of brands are so focused on getting on shelf that they don’t spend enough energy getting off shelf,” he contends.

Keeping product moving off the shelf is a priority for the Lemon Perfect flavored water brand. Photo courtesy of Lemon Perfect

Grogg saw the power of velocity as he worked to build the Kashi brand at Kellogg earlier in his career. “At Kashi, we had amazing velocity. It made selling new accounts so easy,” he says. “If you’re top of the heap on velocity, that next account is going to pick you up.” Unfortunately, Grogg says, “a lot of brands—and some investors—are enamored of getting that new account instead of winning where they’re already playing.”

The velocity-versus-distribution lesson is one that Yanni Hufnagel, founder of cold-pressed water company Lemon Perfect, a startup Grogg has invested in, has taken to heart.

“I think companies now are certainly hearing from investors that they need to have a little more focus on profitability.”

“We talk a lot about the idea of focus and the idea of being a mile deep and an inch wide,” says Hufnagel. “For us, it’s about concentrating in core geographies or core retailers, and establishing a compelling data story or velocity story in those geographies or with those retailers and then using that to move out to build the brand elsewhere.”

8. Sweating the supply chain is critical.

As the COVID-19 pandemic has shown, supply chains are complex and managing them can be challenging. Grogg says he’s found that many founders lack the requisite skill sets.

“It’s not sexy,” says Grogg. “It’s a lot of grinding, detail work, and many, many founders are not good at that part of it.”

“Supply chain can be very tricky,” Lackey agrees. “I’ve seen people get very into the development of the product and the package itself but not pay attention to service levels and the supply chain.”

“I fundamentally believe that the food industry is a supply chain industry. There’s a lot that goes into it, and it’s super complicated.”

Emily Darchuk, whose Wheyward Spirit startup launched the eponymous specialty spirit this past fall, says her years of experience as a product developer with companies including WhiteWave and Coca-Cola allowed her to develop the supply chain expertise she needed for her business.

“My past life had me working with co-packers across the country,” she says. So even while her specialty spirit product was at the conceptual stage, “I was thinking, how is it going to scale up?” She recognized from the start that “all of those decisions that I [was] making really early, they’re going to have to roll up into something that’s operationally successful.”

“So many founders are so driven by selling and the mission side of the brand or whatever it is that motivates them, and most founders don’t really love all the stuff that it takes to get it made,” Grogg continues. “We’ve had companies that launch, and they come to us, and they’re losing money, and they don’t know why. They don’t understand their cost of goods, they don’t understand all the links in the chain . . . so they’re not pricing it [the product] properly.

“Hey, it’s easy to sell a lot if you’re selling it way below the right price,” he notes. “Misunderstanding and mismanagement of the supply chain is a really big issue.”

9. Fundraising finesse is a must.

Finally, sometimes overlooked, but essential for most startups, is the ability to raise money to fund growth.

“You have to be able to have a really good proposal for how you need to go from equity investment to driving value for the shareholders,” says Greven. To raise funds, Krishnan counsels, entrepreneurs must be able to demonstrate a solid understanding of their business’s key metrics, including the size of the total addressable market, their product’s gross margin, its competitive positioning, and the business’s capital requirements.

“The idea could be great, but if you haven’t thought through how you’re going to actualize it, it doesn’t really matter.”

“That convergence of a big market opportunity [and] compelling and fast-improving unit economics—that’s the formula for investor enthusiasm,” says Hufnagel of Lemon Perfect.

Even companies that initially are successful at wooing investors can run into problems if they can’t show that they’ve made good use of the funds, Streiler points out. Investors want to see a detailed financial roadmap before they’re willing to get their checkbooks out for subsequent funding rounds.

“It’s just important to lay out this series of milestones and make sure you’re meeting them before you’re ready to raise money [again],” says Streiler. Completion of market testing and product validation, a proven production process, cost-reduction strategies: “these are tangible milestones that investors want to see as validation of progress before they’re willing to keep investing,” he notes.

What’s more, the investment dynamic has shifted in the past couple of years, says Grogg. “It’s certainly more in vogue now for founders to be more fiscally responsible than it was a few years ago, where it was just grow as fast as you can at any cost and the money will be there.

“Now investors really want to believe that there’s an opportunity for this company to make a profit much earlier than before,” says Grogg. “It used to be, oh well, make a profit at $100 million. And now it’s more like I want to see you break even at $5 million and be profitable at $10 million and be responsible with your margins.”

Startup Experts Eye the Future

What’s the near-term opportunity forecast for entrepreneurs?

Sanjeev Krishnan, chief investment officer and managing director of S2G Ventures, believes that the current era of digital transformation, which has accelerated during the COVID-19 pandemic, bodes well for entrepreneurship opportunities. He points out that, historically, industries have experienced the greatest disruption when they are digitized.

“If I think about what channel digitization means in grocery and food, it’s going to create enormous opportunity for entrepreneurship,” says Krishnan. “Suddenly, the barriers to distribution are lowered, your ability to understand your consumer is much more significant, and it’s really going to create a lot more tailwinds for small and medium-sized brands to enter the marketplace [and] to find their niche to develop their business.”

The pandemic period has been challenging for startups trying to break into the market because many retailers delayed category reviews, opting to “focus on selling what was available versus bringing in a lot of innovation,” Krishnan notes. But he sees that changing post-pandemic. “I think as the vaccine develops and we hopefully have a better handle on the pandemic . . . I see a lot of opportunity in 2022 for a significant growth in innovation again.”

Jeff Grogg, managing director of food industry consultancy JPG Resources, is more measured in his forecast.“I think it’s going to get a little harder to hit big home runs right away because I think money’s going to be a little tighter, and I think the shelf is going to constrict because retailers are reducing SKUs and getting more aggressive on their own [brands],” he says. “I think entrepreneurs are going to have to be really savvy about finding their niche and be laser-focused on delivering value to that target consumer and not getting distracted by trying to do everything.

“But,” he adds, “we also see that there’s continued consumer fragmentation, and we think that continues to create opportunities for innovation.”

Online Exclusive:

Read more startup founders’ stories in the online version of the March issue at ift.org/news-and-publications/food-technology-magazine.

Authors

-

Mary Ellen Kuhn Executive Editor

Mary Ellen Kuhn, executive editor and assistant director of publications, oversees the editorial content of Food Technology magazine.

Categories

-

Food Business Trends

-

Innovation and Insights

-

Startups and New Ventures

-

Supply Chain Management

-

Food Technology Magazine